A quick look at momentum investing

Momentum investing is a strategy where you pick stocks that have shown higher returns in the recent past and hold onto them for a set period. The idea (or hope) is that these stocks will continue to outperform the market for a while.

It’s not just about randomly buying stocks that have done well. Think of it as following a rule or a formula. You apply this formula to your entire investing universe to filter out stocks with high momentum. You then systematically assign weights to them and buy them. After a pre-decided period, you rebalance the entire portfolio, and the cycle restarts.

You decide on this entire strategy by checking if it has worked in the past. And I don’t mean for just a year or two—ideally, you want more than 15 years of history.

Momentum investing is meant to be disciplined. There’s no chaos or guesswork involved. It’s quantitative and aims to remove emotions from investing. I quite like it.

I first came across momentum as a strategy almost six years ago, when I was in college. Over time, I've delved deeper into it, so I thought I'd quickly introduce it to those of you who are relatively new to it.

Disclaimer: This article is provided for informational and educational purposes only. It is not intended to constitute financial, or investment advice. Readers should not construe any of the information provided as a recommendation for any investment or financial decision.

1. Does it work?

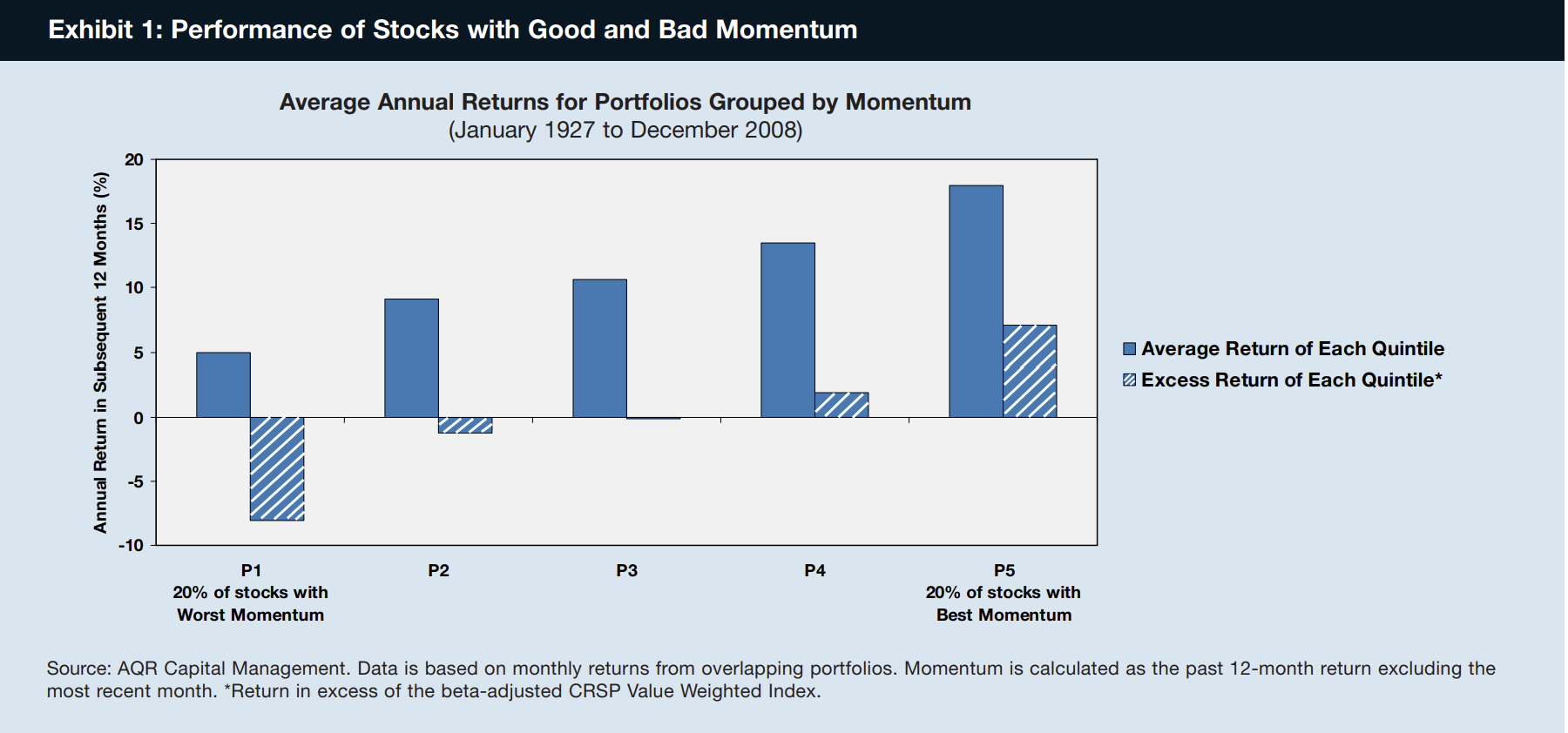

More than 3 decades of research has gone into momentum as a strategy and we know for a fact that it has has generated excess returns in the past.

The hedge fund AQR has done some incredible work on factor investing. Here is an image from their paper titled “The Case for Momentum Investing.”

And the beauty of momentum is that it is not restricted to select countries. Due to its success, even NSE has come out with momentum indices.

For instance the Nifty 200 Momentum 30 is a strategic index released by NSE that has beaten the Nifty 200 benchmark in its 15 year back test. Over time NSE has released more momentum based indices.

What’s more, we now have multiple passive index funds and ETFs that attempt to replicate these indices. We even have mutual funds following momentum as a strategy.

I don’t intend to paint a picture that momentum cannot underperform. Of course it can and has. If you take shorter time periods like an year or two, momentum has underperformed the index in the past.

However, when you extend the time horizon, momentum investing tends to perform well. As the investment firm Capitalmind notes: “Even our backtests show that, on a one-year rolling basis, momentum investing trails the benchmark Nifty 30% of the time. Over longer holding periods, the probability of underperformance drops significantly, but that doesn’t change the fact that for nearly a third of the time, returns will trail the index.”

2. How is momentum calculated?

While a lot may go into running a momentum fund, lets focus on three crucial decisions. Calculating the score, assigning the weights and deciding when to rebalance the portfolio.

Calculating the score

There are different methods to measure momentum. I thought I’d run you through some of the popular ones.

In the 1990s, two professors from UCLA, Narasimham Jegadeesh and Sheridan Titman, published a ground-breaking paper titled "Returns to Buying Winners and Selling Losers." This paper was one of the earliest research works on momentum as a factor. In the conclusion of that paper they wrote:

“Trading strategies that buy past winners and sell past losers realize significant abnormal returns over the 1965 to 1989 period. For example, the strategy we examine in most detail, which selects stocks based on their past 6-month returns and holds them for 6 months, realizes a compounded excess return of 12.01% per year on average.” So they looked at 6 month returns across their investing universe with the simple idea that the higher the return, the higher the momentum & vice versa.

Over time, investors have continually sought to improve methods for calculating momentum. Currently momentum is often defined as the performance of a stock or asset over the past 12 months, with the most recent month excluded.

In a great article by the investing team at Capitalmind, multiple momentum back-tests are presented, showcasing ongoing revisions in how momentum is measured. Beyond absolute returns, they highlight two notable variations:

The momentum score is calculated by taking the percentage of up-days in the last 252 trading days and multiplying that by the absolute return. (Absolute return over an year I think)

Another approach to quantifying momentum involves taking the absolute excess return over the last 52 weeks and dividing it by the annualized standard deviation of daily price movements, similar to a Sharpe ratio. (Again higher the ratio, higher the momentum & vice versa)

In fact, the NSE indices are also based on volatility adjusted momentum scores. As written in the whitepaper “The normalised momentum score is based on 6-month and 12-month price return, adjusted for its daily price return volatility.”

(The scores can be normalized using Z scores)

Assigning Weights

Once a momentum fund has selected its stocks based on momentum scores, the next step is to determine how to allocate weights to each stock. There are several methods to consider, including the following:

Equal Weight: In this approach, if the portfolio consists of 30 stocks, you simply invest an equal amount in each of the 30 stocks.

Market Capitalization Weight: Alternatively, you could weight the stocks by their free float market capitalization. Larger companies with higher market caps would receive a larger weight in the portfolio.

Momentum Score Weight: Another method is to base the weights on the momentum scores themselves. Stocks with the highest momentum scores get a higher weight, while those with lower scores receive less. You could combine two methods too. For example, the Nifty 200 Momentum 30 Index calculates stock weights by multiplying the free float market cap with the normalized momentum score of each stock.

No matter what method is used, risk management is crucial. For example, if the metals sector is experiencing a rally, you might end up with a large number of metal stocks in your portfolio. However, you might not want to take crazy exposure to a single sector. To address this, you could implement provisions to limit sector exposure. It’s important that such rules are predetermined and integrated into your strategy from the outset. Regardless of the method used, the key is to maintain a systematic approach rather than relying on random weights.

Deciding on the Rebalance Period

The rebalance period for a momentum fund is a crucial decision. For example, the Nifty 200 Momentum 30 Index is rebalanced every six months. However, some strategies may choose monthly rebalancing based on the results of their back-tests.

It's important to consider both the level of portfolio churn and the tax implications associated with rebalancing. Frequent rebalancing can lead to higher transaction costs and potential tax consequences, so finding a balance that aligns with the fund's objectives and minimizes unnecessary turnover is key.

3. Why does momentum work?

While there is no consensus on why momentum works, a few potential reasons are commonly discussed. One that I personally find compelling is the Bandwagon Effect.

Essentially, the more people see a stock performing well, the more they want to jump on the bandwagon, pushing prices even higher. Conversely, if a stock is performing poorly, more investors might avoid it, causing prices to fall further. This behaviour can lead to significant price run-ups or -downs as more investors follow the trend, further driving the price in that direction. These trends can continue for extended periods until they eventually correct. Historical examples of the Bandwagon Effect include the technology bubble of the late 1990s.

Another reason why momentum works could be the delay in reactions to information. Different investors—such as traders versus long-term investors—receive news from varying sources and react to it over different time horizons. Additionally, the behavioural phenomenon of anchoring and adjustment means that individuals often update their views only partially when faced with new information, gradually accepting its full impact. This slow reaction to news can create momentum, as prices adjust more slowly than the information would suggest.

Whatever the reason, it seems to be working for the past few decades. (And here’s hoping it continues)

There’s tons to read on momentum, if you are interested. A few suggestions -

AQR Paper - Facts, fiction & momentum investing

Capitalmind Article - Does Momentum work in India?

Whitepaper by NSE on the Nifty 200 Momentum 30 index

Whitepaper by Rajan Raju & Chandrasekharan titled - Implementing a Systematic Long-only Momentum Strategy: Evidence From India

That’s all for now. Thanks for reading

Cover image taken from Unsplash by Sunder Muthukumaran.