India, FIIs, and Market Noise: A Reality Check

Adding some context to the noise

Lately, the news in India has been dominated by discussions about Foreign Institutional Investors (FIIs) exiting the market. Much of this is being attributed to the weakening of the rupee against the dollar and concerns over whether post-tax returns are sufficient for FIIs to continue investing in India.

Let me clarify upfront that I don’t have a definite answer for why we’re seeing such a sell-off. While these concerns are certainly valid and warrant attention, I believe the conversation needs some more context.

MSCI ACWI: A Reality Check on India's Weight

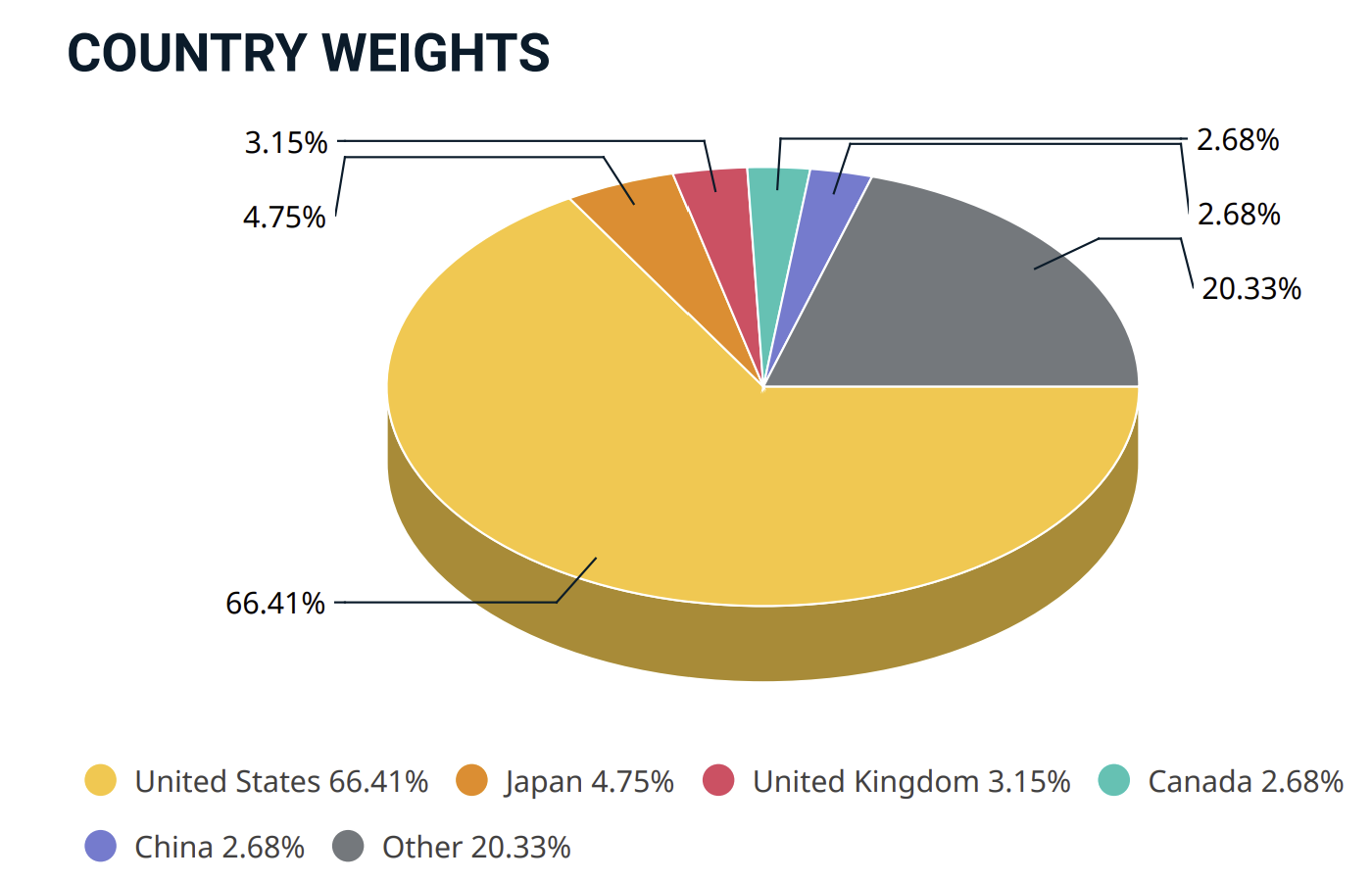

Let’s take a look at the MSCI All Country World Index (MSCI ACWI)—a widely tracked global equity benchmark. It captures large and midcap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries (as of January 2025). The index provides a useful lens to assess India's relative significance in global benchmarks.

The U.S. alone makes up nearly 66% of the index. This underscores a fundamental reality: for a U.S.-based allocator managing global exposure, the primary focus is always on the U.S. market. The discussions revolve around whether to be overweight or underweight the U.S., which sectors to prioritize, and how to balance factor exposures. Naturally, this takes up most of their attention.

India remains a niche allocation rather than a core holding for most global institutional investors. Its weight may be around 2% in the benchmark.

So is that bad sign for India? No. Not at all. Lets look at India for a second.

Still Young? Yes, and it should remain so for at least the next 25 years.

Investment Grade? One of the few countries that is both young and rated investment grade—at least by Moody’s.

Fiscal Deficit? Considered manageable, though always a point of discussion.

Political Stability? The last decade has demonstrated consistency. Even before that, India had a stable democratic framework. The 2029 elections will be interesting to watch.

Growth? Not spectacular recently, but stable. Given global uncertainty, “alright” growth is still better than most alternatives.

Valuations? Have come off recently but far from the cheapest market in the world.

It’s not as if FIIs don’t understand this. In fact, we as Indians almost take everything mentioned above for granted. We don’t actively look at global markets to invest in because India itself has been a great market. That is not the case for much of the world.

Over the last 20 years, the Rupee has depreciated by a CAGR of almost 3.5%, relative to the Dollar. Despite that the before tax return over 20 years (as of 25th Feb 2025) is greater than the SPY. India is probably the best performing market over the last twenty years, and is in the Top 20, even when you look at the last 10 years.

While factors like the rupee, taxes, and market performance play a role in FII decisions, it’s crucial to recognize that not everything FIIs do is because of India itself. As mentioned before, as of now, the most significant decision for a global allocator is not whether they are overexposed or underexposed to India, but rather how they manage their overall portfolio—which, fortunately or unfortunately, often means worrying about their U.S. exposure first.

If you made it so far, thanks for reading. Do consider subscribing if you have not yet.

Disclaimer: This article is a thought piece and is for informational purposes only. It should not be construed as financial or investment advice. Readers should conduct their own research or consult a professional before making any investment decisions.

I wonder whether this is just a function of the breakdown of the postwar order? As transatlantic consensus crumbles and the spectre of populism haunts the west, are most large institution choosing to be more insular?